- What Financial Independence Actually Means

- Why This Conversation Is Different in the Philippines

- Our Personal Financial Independence Journey

- How to Calculate Your Financial Independence Number

- The Saving Rate Is the Lever You Can Actually Pull

- Start Your Financial Independence Journey

- The FIRE Movement, Filipino Edition

- Where Filipinos Invest for Financial Independence

- What Are Some Risks to Prepare For When Chasing Financial Independence?

- Some Practical Steps to Start

- The Part No One Talks About: The Psychology of Staying Invested

- Frequently Asked Questions (FAQs)

- The Bottom Line

Not a lot of financial independence articles out there work for the Filipino context. So, I wrote this full guide, sharing all I’ve learned so far as a thirty-five-year-old (at the time of this writing) working towards a life where my family never has to worry about money ever again.

There’s a conversation most Filipinos have at some point, usually in their 30s, sometimes in their 40s, occasionally after a really bad Monday. It goes something like, “How I wish I never had to work to survive.”

The answer to that burning pain point is financial independence. We’ve been taught that more hustle, a second job, a business, is the only way to be free from financial stress. But what we actually need is a new goal and a different relationship to money entirely.

I hope this blog will explain for you what financial independence actually means, how Filipinos calculate it, why the standard advice often fails us, and what you can realistically do about it. So, take time to read it.

What Financial Independence Actually Means

Financial independence is the point where your living expenses are covered by income that doesn’t require you to show up anywhere.

To get there, you’ll need a collection of assets that you can use to generate enough cash each month to pay for your life. You can still work after that point, and many people do. But the big difference is that you work because you want to, not because the bills are coming.

Financial independence is very different from being rich. A person earning ₱500,000 a month but spending ₱490,000 is not financially independent. A person living on ₱30,000 a month with ₱9 million invested probably is. What matters are the gap between your passive income and expenses, and your reason for working.

Most people work because they have to. People with financial independence work because they want to. In his book, Psychology of Money, Morgan Housel defines independence as the ultimate freedom to control your own time, describing the ability to do what you want

Financial Independence is also different from financial freedom, which a term that gets used interchangeably but means something less specific.

We usually use financial freedom to describe what it’s like when you’re managing well, not stressed about money, and maybe out of debt.

However, financial independence means work is genuinely optional, meaning you still have enough money coming in because your assets work for you, not the other way around.

Why This Conversation Is Different in the Philippines

Most financial independence content is written for Americans with 401(k) accounts, dollar salaries, and a very different tax structure. Their math doesn’t translate cleanly here.

A few things make the Filipino context distinct:

1) Family obligations

For most Filipino families, a handful of employed children quietly fund the education of two siblings, a parent’s medical bills, and sometimes the groceries for an extended household. We’ve built a breadwinner culture, where a chosen few carry the financial burden of providing for everyone. This makes financial relief extremely hard for them.

According to a recent survey, many of today’s young Filipinos expect to become primary providers for their families.

Your real monthly expense isn’t what you spend on yourself. Your financial independence (FI) number needs to account for the people you’re responsible for. Ignoring this produces a plan that collapses the moment a family member gets sick.

2) OFW money

The Philippines receives among the highest remittances in Southeast Asia, reaching over $35 billion in 2025 alone. But remittance is consumption income, not investment income.

Money sent home gets spent. But it means millions of Filipinos spend decades earning well and building very little, or sometimes never building at all.

3) Informal income

Freelancers, small business owners, online sellers, content creators are a huge portion of the Philippine workforce that earns without a payslip.

That’s not a problem in itself, but the financial system is not built for it. Banks won’t easily lend to you. Structured retirement savings are harder to access. The discipline has to come from within, because the institutional scaffolding isn’t there.

4) Inflation eats harder when you earn in pesos

The peso has lost significant purchasing power over the past decade. If your savings are parked in a traditional bank savings account earning 0.10% interest while inflation runs at 4–6%, you’re getting poorer in real terms every year.

The math on this is brutal, and most Filipinos don’t see it because the nominal peso amount in their passbook keeps going up.

Our Personal Financial Independence Journey

My wife Ces and I run an online business from home called Block Ten Strategy. It provides good income for me, my wife Ces, and our two daughters, Alexa and Sam. For a long time, retirement was something we knew we should think about, just not yet.

“Not yet” has a way of becoming never.

The shift happened when a wealth manager asked us a simple question: do you have a million pesos? We did, and it was sitting in accounts barely growing. He introduced us to Coast FI (more on this later), and the math changed everything.

The plan was to take that ₱1 million and dollar-cost-average into the S&P 500. After that, we stop contributing entirely and let compounding do the rest. At a 10% historical annual return, that ₱1 million grows to approximately ₱20 million by the time we’re 65.

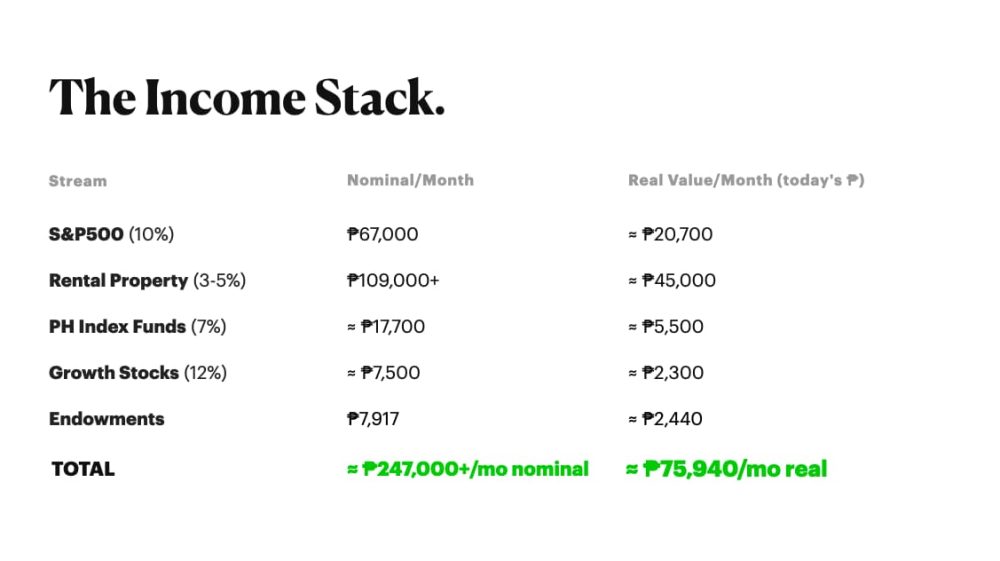

The piece that makes this work in the Philippine context is geo-arbitrage. We invest in dollar-denominated global markets but spend in pesos in the province. That gap is what turns a ₱20 million portfolio into a genuinely comfortable retirement — roughly ₱66,000 a month in passive income under the 4% withdrawal rule.

We’re on track to finish that sprint by 2027.

On top of that, we’ve also invested in rental properties. They’re on mortgages now, and we’re using the revenue to continue building an investment flywheel that will strengthen our financial independence roadmap.

I explain more about that strategy in the video below:

And the S&P 500 is just one piece. Our full income stacks at retirement projects to about ₱75,940/month in real peso value (meaning inflation-adjusted) across five streams. Check out the full income stack below.

That’s the target where Alexa and Sam never have to ask how we’re paying the electricity bill.

We grew up without generational wealth. We know what that cost. This is how we make sure it doesn’t cost our kids the same. So, how did we come to all these numbers and strategies? It all starts with knowing one number: your FI number.

How to Calculate Your Financial Independence Number

The standard framework of knowing your financial independence number is called the 4% rule. It comes from the Trinity Study, a 1998 analysis of US market returns, but the logic holds broadly.

Here’s the core idea: if you withdraw 4% of your investment portfolio per year, historical market returns suggest that the portfolio lasts at least 30 years or often longer. Since then, the number has been upgraded to around 4.7% even.

Let’s run some numbers to explain this more. If your household spends ₱480,000 a year (₱40,000/month), your FI number is ₱12,000,000. Once your invested assets hit ₱12 million, withdrawing 4% (₱480,000) covers your expenses. You don’t touch the principal. The portfolio keeps growing. You stop needing a salary.

A few important caveats for the Philippine context:

- A 3% withdrawal rate is safer for early retirees. Even with the 4.7% rule, I would rather be more conservative. If you’re planning to retire at 40 and need the money to last 50 years, not 30, use ₱Annual Expenses × 33 as your target. The 4% rule was built for a 30-year retirement horizon.

- Your FI number should include family obligations. If you’re currently supporting parents or siblings, factor that into your annual expenses. If you stop working, those responsibilities don’t disappear.

- Peso inflation matters. Your ₱12 million in 2025 buys more than your ₱12 million in 2035. Build inflation assumptions into the plan. A rough rule: assume your expenses grow 4% per year and use investment vehicles that outpace that.

The Saving Rate Is the Lever You Can Actually Pull

Your saving rate is simply the percentage of your income you put into investments each month. This will determine how fast you get to financial independence.

A higher saving rate does two things at once.

- It grows your portfolio faster.

- It means your lifestyle is cheaper, which lowers the FI number you’re chasing.

According to some financial experts, this is what the savings and investing math will look like at varying savings rates (estimates)

| Saving Rate | Approximate Years to FI |

| 10% | ~40 years |

| 25% | ~27 years |

| 50% | ~17 years |

| 70% | ~8 years |

(Calculations above assume ~5–7% real investment returns after inflation)

Going from 10% to 25% saves you more than a decade in preparing for financial independence. Most Filipinos, including high earners, will likely save somewhere between 0% and 5% of their income in any given month. The rest goes to lifestyle, family, or consumption.

I hope this doesn’t come across as judgment. I know what it’s like, because we too had our moments where we just simply saved whatever was left at the end of the month (if any was left). We had no savings goals and no real plan.

The single highest-leverage financial decision you can make is to increase your savings rate first and your income after. Because even if you increase your income but keep inflating your lifestyle, you’re not going to inch closer to work optionality.

Start Your Financial Independence Journey

I created this playbook for all Filipinos looking for a financial independence roadmap that works for our context. Download my financial independence guide for Filipinos for free here.

What does a good savings rate look like for a regular Filipino salary?

Let’s use a concrete scenario. Say you earn ₱50,000 a month, roughly the take-home pay of a mid-level professional or a consistent freelancer. You support yourself, send ₱8,000 home to your parents each month, and your personal living expenses run about ₱25,000.

Your actual monthly outflow is ₱33,000. Your available amount to save and invest is ₱17,000. That will give you a saving rate of 34%.

At a 34% saving rate, you’re looking at roughly 22–23 years to full financial independence, assuming 5–7% real returns after inflation.

The numbers are not as impossible as they feel. The math just requires you to start.

The FIRE Movement, Filipino Edition

FIRE stands for Financial Independence, Retire Early. The idea is to accelerate the standard timeline. So, instead of working until 65 years old, you target financial independence in your 40s or even earlier through aggressive saving and investing.

The movement originated in the US but has a growing following in the Philippines, particularly among tech workers, online freelancers, and OFWs with higher disposable income.

There are a few variants, and they matter because they represent different lifestyles:

1) Lean FI

Lean FIRE means reaching FI on a tight budget. Your FI number is lower because your annual expenses are lower — maybe ₱20,000/month instead of ₱50,000. You live simply, own little, and the trade-off is a smaller, more disciplined life in exchange for reaching independence earlier.

For some Filipinos, Lean FIRE is already close to the default, especially those from provinces where the cost of living is genuinely lower. A household in Iloilo or Cagayan de Oro running on ₱25,000/month has an FI target of ₱7.5 million. That’s still significant, but it’s a different mountain than the one Metro Manila expenses require.

2) Fat FI

Fat FIRE means reaching FI with enough to live comfortably. That includes travel, good food, private school for the kids, and so on. In this case, your FI number will be higher. So, you need more time to get there, but you don’t sacrifice lifestyle along the way or after.

For most upper-middle-class Filipino families, Fat FIRE probably looks like ₱80,000–₱150,000/month in today’s expenses, putting the target between ₱24 million and ₱45 million. Achievable, but it requires serious income and serious discipline over a long period.

3) Barista FI

Barista FIRE is semi-retirement. Your portfolio covers most of your expenses, and you work part-time, maybe a small business, consulting, or a side project to cover the rest. You’re not fully out, but you’re not dependent on a job either.

This is probably the most Filipino version of FIRE in practice. A lot of people do this without calling it anything: they hit a point where the passive income covers most bills, and they shift to part-time freelancing or a small sari-sari store, knowing they don’t need it to work out perfectly.

4) Coast FI

Coast FIRE is a milestone in personal finance where you have enough money invested today that, thanks to compound interest, it will grow to cover your entire retirement without you ever contributing another penny. You still work, but only to cover your current living expenses.

This one’s our personal goal. And, as I mentioned earlier, we’re on track to hit coast FIRE by this time next year.

Coast FIRE is the one I want to spend more time on because it’s our personal strategy. In my humble opintion, it’s also the most underrated variant of the FIRE movement.

You still work after that point, but only to cover your current living expenses. The retirement piece is already handled.

Your Coast FI number is the amount you need invested today so that, at your expected average annual return, it grows to your full FI number by your target retirement age — without any additional contributions.

This is how you calculate your Coast FIRE number:

Coast FI Number = FI Number ÷ (1 + annual return rate)^years to retirement

Here’s a concrete example.

Say your full FI number is ₱20 million, and you want to retire at 65. You’re currently 35, so you have 30 years. Using a 10% annual return:

₱20,000,000 ÷ (1.10)^30 = approximately ₱1,150,000

That’s your Coast FI number. Once your portfolio hits ₱1.15 million at age 35, you can stop investing forever and still reach ₱20 million by 65 — assuming historical S&P 500 returns hold.

This is almost exactly the math behind our own plan. One million pesos, invested over 24 months through peso-cost averaging, growing untouched for 30 years.

Why Coast FI works especially well for Filipinos:

The standard FI path assumes you keep investing for 20–30 years straight. That’s hard to sustain when income fluctuates, family obligations spike, or life simply gets in the way. Coast FI compresses the hard part into a shorter, more survivable sprint. Once you hit the number, the pressure is off. You work to live — not to build a retirement fund anymore.

It’s also why starting early matters so much. The younger you are when you hit your Coast FI number, the smaller that number needs to be. A 25-year-old needs a much smaller portfolio to coast to ₱20 million than a 45-year-old does, simply because time compounds longer.

What’s the Best FI Path For Me?

That depends. Only you know the answer to that because financial independence is a personal goal. And we all have different goals.

But as a starting point, here’s how I would compare these paths:

| FI Type | Monthly Lifestyle | Approx. FI Target (PHP) | Timeline | Best For |

|---|---|---|---|---|

| Lean FI | ₱15,000–₱25,000 | ₱4.5M–₱7.5M | 10–15 years | Province-based living, minimalists, single earners |

| Barista FI | ₱25,000–₱45,000 | ₱7.5M–₱13.5M | 15–20 years | Semi-retirees, freelancers, small business owners |

| Fat FI | ₱80,000–₱150,000 | ₱24M–₱45M | 20–30 years | Metro Manila families, dual-income households |

| Coast FI | Any — you just stop contributing | Varies by age and timeline | Short sprint, then coast | Early starters, online earners, OFWs with lump sums |

FI targets based on 25x annual expenses. Timeline estimates assume 5–7% real annual returns after inflation.

Where Filipinos Invest for Financial Independence

The question of where to put the money is a whole separate topic, but broadly: you need your money in assets that grow faster than inflation and compound over time.

A few options that are accessible in the Philippines:

Philippine Stock Exchange (PSX) or index funds. The PSEI has historically returned around 8–12% nominally per year over long periods. Index funds via platforms like COL Financial or ATRAM are lower-cost options than actively managed UITFs.

However, the past few years have been very sideways for the PSE. We’ve not really seen any meaningful growth from Philippine stocks. However, dividend payments are still considerably healthy. We started investing in Philippine stocks in 2016. We have seen some form of growth, but the recent market downturns have practically wiped them all out.

US stocks through local brokers. Some digital brokers and global platforms allow peso-funded access to US equities. Over the past 20 years, the S&P 500 has returned roughly 10% annually in USD. For peso investors, this also provides a natural hedge against peso depreciation.

You can also work with a wealth manager in a country like Singapore, which is the route we took last year. We started moving our

Real estate. Buy-to-rent real estate is a common Filipino path to passive income, though it requires more capital, more management, and is less liquid.

A unit that generates ₱20,000/month net of expenses contributes ₱20,000 toward covering your FI expenses. The challenge is that Philippine property prices have risen faster than rental yields in many areas, compressing returns.

UITFs and bond funds. These are lower-risk but also lower-return. They’re useful as a stability layer in a larger portfolio, but you cannot reach financial independence by parking everything in a bond fund earning 4–5% when inflation is running at the same rate.

We have about 25% of our liquid assets in UITF parked simply to try to beat inflation. So far, they’ve somewhat done that job well, giving us around 5-7% in growth every year.

The core principle: diversify across asset classes, keep fees low, and invest consistently over time rather than trying to time the market.

What Are Some Risks to Prepare For When Chasing Financial Independence?

Financial independence planning has a few failure modes that are specific to the Philippine context and worth naming directly.

1) Healthcare without PhilHealth as a floor

If you retire at 45, you’re self-funding healthcare for potentially 40+ years. Philippine private health insurance costs rise sharply with age. Factor this into your annual expenses at ₱60,000–₱120,000/year for a comprehensive family plan, and plan for that cost to increase as you age.

2) The “one bad event” problem

Major emergencies can crater an FI plan when you don’t have a buffer. Some of them might include a serious illness, a family member who needs extended support, a business that fails, and so on. The recommendation from most financial planners is to keep a 6–12 month emergency fund completely separate from your investment portfolio, in liquid, low-risk accounts.

3) Sequence of returns risk

The fix is to keep 1–2 years of expenses in cash or near-cash assets when you hit your FI number, so you’re not forced to sell investments at a loss during a downturn.

If the market drops significantly in the first few years of your retirement, and you’re withdrawing from the portfolio at the same time, you can permanently damage your ability to recover.

4) Lifestyle inflation

Most people underestimate how much their expenses grow as their income grows. The freelancer earning ₱50,000/month lives very differently from the one earning ₱200,000/month. If your saving rate stays the same but your absolute spend rises dramatically, you’re running in place. Track actual numbers, not percentages.

Some Practical Steps to Start

None of this works without a starting point. Here’s what actually moves the needle:

1. Calculate your real monthly expenses, including family obligations.

Start with what you actually spent last quarter, averaged out. Most people are surprised by this number.

2. Calculate your savings rate.

Take what you saved/invested last month, divide by your gross income. If the answer is under 20%, that’s where to focus.

3. Open an investment account.

You can start with local platforms like COL Financial, GStocks, or GFunds through your local bank. The goal isn’t the perfect portfolio at the start. The goal is to start, not grow.

Treat this like practice because building your financial independence roadmap isn’t just reliant on your math skills. It’s also going to depend on you having the emotional resilience to stay the course even when the markets get rough.

4. Automate contributions.

The most reliable saving strategy is one that doesn’t rely on willpower. Set up automatic transfers to your investment account on payday. Spend what’s left, not what feels comfortable.

5. Calculate your FI number.

Multiply your current annual household expenses (including obligations) by 25–33 depending on your target retirement age. Write the number down somewhere visible. Abstract goals don’t stick; specific numbers do.

6. Build the emergency fund first.

Before you get aggressive with investing, make sure you have 6 months of expenses in a liquid account. Emergencies happen, and pulling from investments at the wrong time is expensive.

7. Protect your income.

Start with life insurance, health insurance, and some form of income replacement protection. Don’t treat your insurance as investments. That’s not what they’re there for. They’re the fence around your plan that keeps one bad event from destroying it.

To learn more about how we started our financial independence journey and began building towards financial independence, check out this free video training I created on my YouTube channel.

The Part No One Talks About: The Psychology of Staying Invested

You can have the right strategy, the right investment vehicle, and the right savings rate, and still blow your financial independence progress right out the door. Because while some people get the math right, their emotions are what fail them.

That’s why I found it really helpful to spend the first year or so of our investment journey dealing with our emotions, not our returns. We started investing at the peak of PSE in 2018, when the market hit about 9,000 in value (the all-time high). Then the market started crashing. That experience taught us how to manage our emotions when our money started losing paper value.

There’s a field called behavioral finance, which is the study of how psychology actually drives financial decisions. Traditional financial theory assumes investors act rationally. But real-world behavior proves otherwise. Most of us (me included) operate on fear, greed, overconfidence, and social pressures, which often override logical decision-making.

We already know what we should do. We just don’t do it. So why is that? Here’s a look at some of the science behind how we think about investing and finance.

Loss Aversion

According to research by Nobel Prize-winning psychologist Daniel Kahneman and Amos Tversky, the torment of a loss is psychologically twice as powerful as an equivalent gain. Their estimates put the loss aversion coefficient at 2.25, meaning losses loom more than twice as large as equivalent gains.

Watching your portfolio drop ₱50,000 feels roughly twice as painful as watching it gain ₱50,000 feels good.

The losses spring to mind more readily than the gains. You might not notice the gradual growth building over time, but a modest drop catches your attention immediately. That’s not weakness, but rather our human wiring.

What Happens When Fear Wins

In March 2020, the S&P 500 plummeted over 34% in just 23 trading days. Many investors panicked and sold, locking in their losses permanently. The same thing happened with the Philippine Stock Exchange. We saw our investments drop by as much as half in a matter of one week.

But the S&P500 then gained 45% in just three months after the March low (took longer for the PSE. Sigh). Investors who waited for “clarity” missed some of the best days in market history. Those who stayed invested or even bought more during the dip benefited from the full recovery.

They didn’t have better information. They had better emotional discipline.

The Two Enemies of Every Long-Term Investor

There are two enemies to investing when you’re building towards financial indepdendence:

Fear shows up when your portfolio turns red. It tells you to pull out before it gets worse. It feels rational in the moment. It almost never is.

Greed shows up in Viber group chats promising 30% monthly returns. In crypto tips from a cousin who “made it big.” In the urge to abandon a boring index fund because someone else seems to be getting richer faster. Greed leads to overconfidence, where investors take on excessive risks in pursuit of higher returns while ignoring the potential for losses.

Both pull you off the plan. In the Philippines, the social layer makes this harder — group chats flood with opinions during every market dip, and the cultural pressure to lend from your portfolio when family needs help is real and constant.

What Does Emotional Discipline Actually Look Like?

Here’s what you want to work towards.

- Automate contributions. When the transfer happens on payday automatically, you remove the emotional decision entirely.

- Don’t check your portfolio daily. Frequent checking amplifies loss aversion. A portfolio reviewed monthly feels calmer than one checked every morning — same numbers, completely different psychological experience.

- Write your strategy down before a crash happens. When you’re calm, write one sentence: “If my portfolio drops 30%, I will not sell.” Your future panicked self will need it.

- Separate your investment account from your emergency fund. If family emergencies can reach your investments, they will. Make the account structurally harder to access — different platform, different institution, deliberate friction to withdraw.

It’ll take time to build emotional fortitude, and my personal opinion (not sure on the research behind it yet, but trying to learn more about this) is that most people never get to a point of full emotional discipline. But it’s more about progress over perfection.

We’ll all make emotional mistakes when investing. So, no judgment here. I’ve made my own fair share of mistakes, too. But what I try to do is understand my personal money mindsets more and continue working towards making more good financial decisions even when my emotions pull me in another direction.

Frequently Asked Questions (FAQs)

Is financial independence the same as financial freedom?

Not exactly. Financial freedom usually means you’re managing money well and feel less stressed about it. You might still have a job, but money isn’t a constant source of anxiety.

Financial independence is more specific: your passive income covers your living expenses, and employment is genuinely optional. Financial independence usually implies financial freedom, but the reverse isn’t always true.

Can you be financially independent without a job?

Yes, that’s the whole point. Once your investments or passive income cover your expenses, you don’t need employment income. Many people reach FI and choose to keep working, but in a different capacity: consulting, passion projects, part-time work. The key shift is that they’re no longer financially required to do so.

What does FIRE stand for?

FIRE stands for Financial Independence, Retire Early. It refers to a movement of people who aggressively save and invest with the goal of reaching financial independence well before traditional retirement age.

What is the 4% rule?

The 4% rule is a guideline for sustainable portfolio withdrawals in retirement. It says that withdrawing 4% of your portfolio annually has historically allowed a portfolio to last at least 30 years. Working backwards, your FI number is 25 times your annual expenses. For longer retirement timelines, a more conservative 3% withdrawal rate (33x expenses) is often recommended.

How much do I need to be financially independent in the Philippines?

It depends on your expenses and how many people you support. A single person living on ₱30,000/month needs roughly ₱9 million invested. A family of four spending ₱80,000/month, including support for parents, needs closer to ₱24–30 million. The number feels large until you start calculating how long consistent investing actually takes to get there.

At what age can Filipinos realistically reach financial independence?

With a 50% saving rate and disciplined investing, 15–20 years from when you start is realistic. Start at 25 with serious intent and you could hit it by 45. Start at 35 and it’s 55. Start at 45 and you’re looking at the standard retirement window. The variable that matters most isn’t your starting salary — it’s when you actually begin.

Do I need to pay taxes on my investments?

Yes, because as the cliche goes, there are only two things sure in life: death and taxes.

But the specifics depend on what you’re investing in, and this is one area where a conversation with a licensed tax professional is genuinely worth the time. The rules are more nuanced than most FI articles let on, and getting it wrong can quietly eat into returns you’ve spent years building.

That said, here’s a general lay of the land:

Stock market (PSE): Share transactions are subject to a 6/10 of 1% stock transaction tax on the gross selling price, paid every time you sell. Capital gains from the sale of listed shares are generally exempt from capital gains tax, but this only applies to shares traded through the exchange.

US stocks and global index funds: This is where it gets more complex. Dividends from US-listed stocks are typically subject to a 30% US withholding tax for non-resident aliens, though this can sometimes be reduced under tax treaties. How your gains are treated on the Philippine side depends on how you’re investing, through a local broker, a foreign platform, or a wealth manager in another country.

Real estate: The sale of real estate in the Philippines is subject to a 6% capital gains tax on the gross selling price or zonal value, whichever is higher. There’s also a documentary stamp tax and other transfer costs to factor in.

UITFs and mutual funds: Generally, gains are already net of taxes at the fund level, but the structure varies. Always check the fund’s KIID (Key Investor Information Document) for specifics.

Taxes on investments are real, and ignoring them when calculating your FI number means your projections will be optimistic. A fee-only financial advisor or a CPA familiar with investment taxation can help you build a tax-efficient strategy, especially if you’re investing across multiple asset classes or through foreign platforms.

The Bottom Line

Financial independence is not a wealthy-person goal. It should be everyone’s goal. While the math is straightforward (spend less than you earn, invest the difference in assets that grow faster than inflation), the real challenge is starting. We wait for all circumstances to be perfect: having overflowing cash, low expenses, no emergencies, perfect returns, and no down markets. That never happens.

If you wait for the perfect entry to start, you’ll likely start too late. But if you start as early as possible, and wait long enough for compounding to close the gap. The best time to start was 10 years ago. The second best time is now, with a specific number and an actual investment account.

Disclaimer: This article is for informational purposes only and does not constitute financial advice. Please consult a licensed financial advisor before making investment decisions.